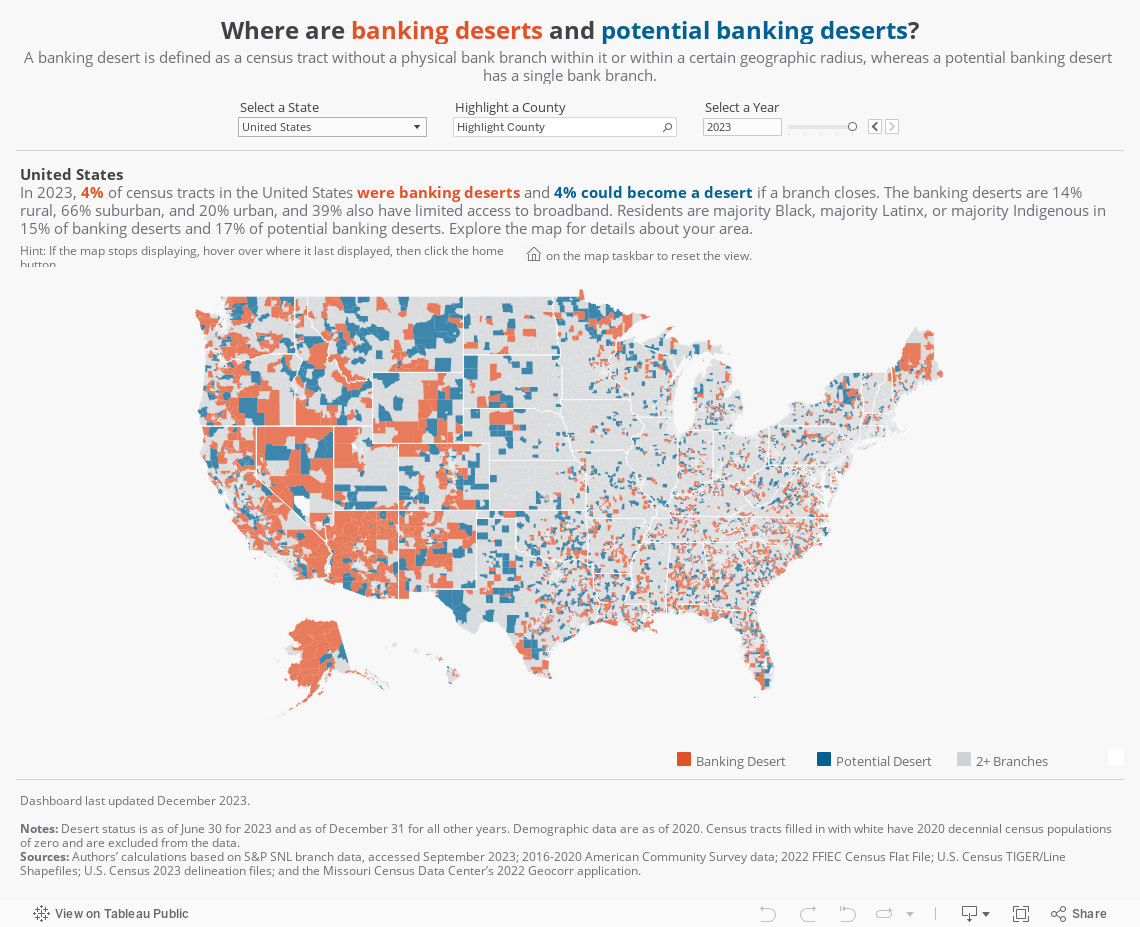

Banking Deserts Dashboard

Page last updated: November 3, 2025

Drying up: The decline of bank branches in the United States

The number of bank branches across the United States is declining. While the popularity of online banking has grown, physical banking still plays an important role for many consumers. Lack of access to banking services can mean losing opportunities to improve financial health and build wealth.

That’s why it’s important to identify communities that have few or no bank branches nearby. One way to do that? Tracking banking deserts.

How do you define a banking desert?

A banking desert is a census tract without a bank branch located within it or within a certain radius from its population center. That radius is determined by the type of community:

- 2 miles for urban communities

- 5 miles for suburban communities

- 10 miles for rural communities.

A potential banking desert is a census tract that can become a banking desert if one bank branch closes.

2019: Three branches in radius

2020: Potential banking desert

2021: Banking desert

Census tract 3209.03 in Indianapolis, Indiana, with its two-mile radius, and branches nearby.

Sources: S&P SNL branch data and U.S. Census TIGER/Line Shapefiles.

Keep reading for answers to frequently asked questions about banking deserts.

Why do banking deserts matter to financial inclusion?

Research suggests bank branches’ presence in lower-income communities is linked to more mortgage originations and lower interest rates. Declining access to traditional banking services might also drive consumers to alternative financial services like payday lenders and check-cashing services that can raise the overall cost of banking and inhibit opportunities for saving.

Living in a banking desert may impact some consumers more than others. There’s still a high demand for access to a physical bank branch with a teller for the following demographics:

- Lower-income consumers

- Older adults

- People living with disabilities

- Rural consumers

While many financial institutions offer online and mobile banking, consumers need three key elements to use these services:

- A modern digital device

- Internet access

- The ability to navigate websites and apps

Unfortunately, home broadband adoption remains out of reach for many lower-income, rural, and older populations, as well as people of color. Without true digital inclusion–high-speed internet, devices, and digital skills–these consumers may find it challenging to fully embrace online banking services.

How can I identify a banking desert in my community?

The Banking Deserts Dashboard can help you quickly identify banking deserts and potential banking deserts. It has census tract-level data on physical bank branch availability within all 50 states from 2019–2025. Identifying communities with limited access to physical bank branches can help inform solutions for better serving the financial and banking needs of their residents.

Banking Deserts Dashboard

The Banking Deserts Dashboard is intended for informational and educational purposes.

Have a question or comment? Contact us.

Want to explore banking desert data further?

(40MB .zip)

(.pdf)

Banking Desert FAQs

A banking desert is defined as a census tract without a physical bank branch within a certain geographic radius from its population center or within the tract itself. That radius is determined by the type of community: 2 miles for urban communities, 5 miles for suburban communities, and 10 miles for rural communities. This definition is based on “areas with very low branch access” in the Interagency Notice of Proposed Rulemaking to Implement the CRA.

A potential banking desert is defined as a census tract that will become a banking desert if one bank branch closes, a definition based on “areas with low branch access” in the Interagency Notice of Proposed Rulemaking to Implement the CRA.

Tracts where more than 21.5% of households did not have access to broadband internet in the 2016-2020 American Community Survey (ACS) are considered tracts with limited access to broadband. Those tracts are among the top 25% for the share of households without access.

A census tract is considered low- and moderate-income (LMI) if its 2016-2020 ACS median family income is below 80% of the area median family income and is considered middle- and upper-income (MUI) if the 2016-2020 ACS median family income is greater than or equal to 80%. Values are not available for tracts with insufficient income information.

A census tract is urban if its population lies primarily within a metropolitan statistical area (MSA) and a principal city of its MSA. It is suburban if its population lies primarily within an MSA but not within the principal cities of its MSA. The tract is rural if its population does not lie primarily within an MSA. We use US Census 2023 delineation files for principal cities of MSAs.

A census tract has a majority race/ethnicity if more than half of its 2016-2020 ACS population shares the same race or ethnicity. If no race/ethnicity makes up more than half of a tract’s population, it is labeled as having “no predominant race.” A tract where most residents are people of color is one in which more than half of its population is Hispanic or non-white.

The dashboard data will be updated annually. To receive emails about future updates of the dashboard and other Fed Communities content, sign up for our newsletter.

Fed Communities recently published an article exploring how community development financial institutions (CDFIs) are stepping in to help fill the gaps. The Philadelphia Fed has recently published a report that analyzes this data, and has also recently published a deeper dive of banking deserts in the Federal Reserve Third District states of Pennsylvania, New Jersey, and Delaware.

Please note that the Federal Reserve is not a grantmaking organization. Additionally, the Fed does not maintain grant money or any other type of funds or accounts for individuals.

Banking Desert Dashboard Methodology

We calculate the desert status of census tracts using bank branch locations from S&P Global Market Intelligence SNL US Bank Branch Data Set (“S&P SNL branch data”). The sample of branches used are inclusive of brick-and-mortar, non-in-store, full service, and retail branches. We include all types of banks and credit unions, but not Community Development Financial Institutions (CDFIs).

We also make additional data-cleaning decisions in constructing the sample of bank branches. First, we remove cases where the branch status is “closed” but the closed date is missing. We also remove cases where the branch status is “active,” but the closed date is populated.

Second, we identify a small sample of branches likely to be duplicated (3%). These are cases in which the institution company name, first address line, and city are the same as one or more other observations with overlapping open/closed dates. We then decide which observation is most likely accurate within each group of duplicates through a series of decisions that lead us to drop about half of the 3% of observations identified as duplicates.

Finally, while approximately 15% of the remaining observations are missing open dates, we include those observations to avoid overestimating the number of banking deserts. A cross-examination of Summary of Deposits (SOD) data from the Federal Deposit Insurance Corporation, the main data source used to construct the non-credit union portion of the S&P SNL branch data, revealed that 99.4% of bank branch cases with missing open dates that we identify as having stayed open at the end of 2019 were identified and active in the SOD data as of June 2019. Thus, we assume with great confidence that these branches were open in 2019.

We use the latitude and longitude of bank branches in the S&P SNL branch data to geocode each branch to 2020 census tracts. We use the 2016–2020 American Community Survey (ACS) data and 2022 FFIEC Census Flat File for relevant census data, US Census TIGER/Line Shapefiles for geographic boundary computations, US Census 2023 delineation files for principal cities of metropolitan statistical areas, and the Missouri Census Data Center’s 2022 Geocorr application for data on population-based tract centroids and areal overlap between tracts and principal city boundaries.

We define banking deserts and potential banking deserts based on the definitions of “areas with very low branch access” and “areas with low branch access,” respectively, introduced in the Interagency Notice of Proposed Rulemaking to Implement the CRA. However, there are two slight differences between our data and methodologies and the interagency data and methodologies: For one, we use a stricter definition of “active branch,” and two, our data are more recent and have been retroactively updated to capture closures that occurred in 2020 and 2021.