A 4-bedroom Minneapolis, Minnesota single-family home acquired from an investor portfolio, renovated and for sale to a buyer earning less than 80 percent of area median income through the City of Minneapolis and Land Bank Twin Cities’ Single-Family Investor-Ownership Intervention Pilot Program.

Photo courtesy of Land Bank Twin Cities.

Single-family rental homes (SFRs) are a vital part of the US rental housing market. These homes can offer renters access to neighborhoods where home prices are out of reach and zoning excludes apartment buildings. But as with all rental housing, the owner’s goals and intentions influence affordability and stability for the tenant.

Investors who buy and rent out single-family homes have come under scrutiny as their share of the SFR market has grown over the past two decades. What impact do investors have on tenants and neighborhoods? And how can the model evolve as more investors center goals such as affordability, preservation, and community control of SFRs?

More than a third of American households rent their homes. While “rental housing” might bring to mind apartments, 35 percent of renter households lived in single-family homes in 2023, according to the American Housing Survey. Certain data sources, including the US Census, count some attached properties, like row houses, townhouses, and duplexes, as single-family homes.

Some renter households prefer a house over an apartment for particular reasons. For one, single-family rental houses are typically larger. In 2023, Census data showed that more than 63 percent of SFRs included three or more bedrooms, versus 11 percent of apartments. SFRs were also more likely to include off-street parking and private outdoor space.

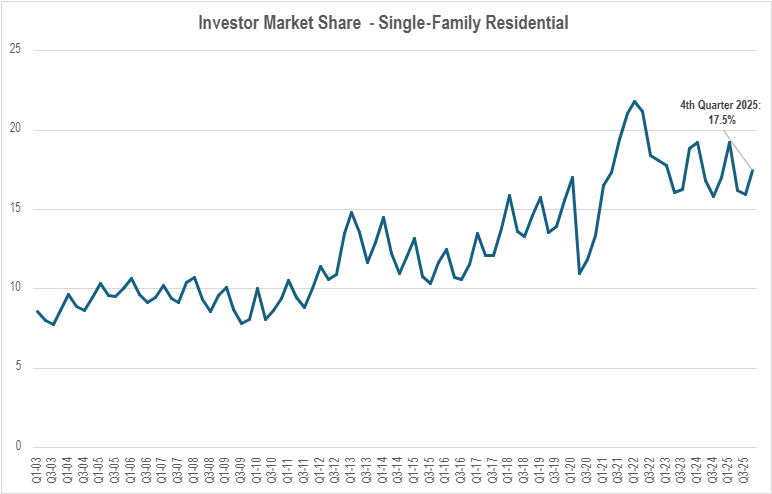

Much recent discussion has revolved around investors buying single-family homes. Investors have gradually increased their SFR ownership share since 2000. Growth was particularly strong around the late-2000s foreclosure crisis and recent pandemic. In a pandemic-era peak, investors bought about 22 percent of single-family houses on the market in early 2022. Their share has dipped into a relative plateau since, with investors purchasing nearly 18 percent of single-family houses in the last quarter of 2025.

Institutional investors—defined here as companies, partnerships, or other entities with more than 100 single-family homes—owned just 3.8 percent of the US single-family rental housing stock in 2022, according to a recent Urban Institute analysis. Investors holding fewer than 100 properties own the overwhelming majority of SFRs.

Concerns over disproportionate investor activity in lower-income neighborhoods

While their overall market share is low, institutional investors have been more significant players in certain places. The Urban Institute analysis found concentrations of institutional holdings in metropolitan areas such as Atlanta, Phoenix, and Dallas. A 2024 Richmond Fed analysis also found higher levels of institutional investor SFR purchasing in the growing Charlotte, North Carolina, market. Rapid population growth and limited housing supply can boost rent levels in Sunbelt areas like these, attracting investor interest.

“Fundamentally, investors are buying homes in places where the rent revenue stream is greater than the cost of ownership,” said Libby Starling, senior community development advisor at the Minneapolis Fed.

“Fundamentally, investors are buying homes in places where the rent revenue stream is greater than the cost of ownership.”

– Libby Starling, Minneapolis Fed

Photo courtesy of Grounded Solutions Network.

Cost of ownership starts with the purchase price, so institutional investors often are interested in lower-priced homes. When regional community leaders raised concerns about investor purchase activity in lower-income areas, where home prices tend to be lower, Federal Reserve researchers examined the data. Their analyses showed disproportionate impacts in some lower-income neighborhoods, particularly during and after the pandemic.

Looking across seven counties in Ohio and Pennsylvania, for example, Cleveland Fed senior policy analyst Matt Klesta found that 79 percent of the census tracts with the highest concentration of investor activity between 2018 and 2024 were low- and moderate-income tracts.

Philadelphia Fed researchers Lei Ding, Sisi Zhang, and Mckenzie Diep found large corporate investors owned significant concentrations of SFRs in lower-income neighborhoods of West and Southwest Philadelphia. Roughly 85 percent of single-family home sales to these investors occurred in low- and moderate-income Philadelphia neighborhoods between 2020 and 2023.

The Minneapolis Fed built an interactive tool to help community leaders and policymakers understand investor activity across the Twin Cities over time. Studying 2022 data, the Minneapolis Fed’s Starling noted disproportionate shares of investor-owned single-family rentals in lower-income neighborhoods and areas heavily affected by foreclosure during the late-2000s housing crisis.

Investors can contribute to righting downturns in the housing market

What these concentrations of investor activity mean for residents of lower-income neighborhoods is not entirely clear. Some studies have found evidence that increased investor activity correlates with increased home prices, rents, and eviction filings.

“It’s important to think about the role investors play when housing markets are not doing well. Properties that go through foreclosure or short sale often have a lot of problems, and people aren’t always well-equipped to be first-time homebuyers of those properties. Investors can have a positive role in stabilizing those markets.”

– Lauren Lambie-Hanson, Philadelphia Fed

Yet some research found that, in part, price and rent increases correlate with large investors buying inexpensive, dilapidated homes and renovating them before renting them out. Their efforts can improve both housing and neighborhood quality. Research also shows that investors have contributed to stabilizing housing markets when demand fluctuates. A 2019 Philadelphia Fed study showed that investor activity during the recovery from the late-2000s housing crisis helped return homes to the market, reducing vacancy rates.

“It’s important to think about the role investors play when housing markets are not doing well,” said Lauren Lambie-Hanson, a special advisor at the Philadelphia Fed and coauthor of the 2019 study. “Properties that go through foreclosure or short sale often have a lot of problems, and people aren’t always well-equipped to be first-time homebuyers of those properties. Investors can have a positive role in stabilizing those markets.”

Given current tight housing supply, large investors also have the financial ability to return needed units quickly to the market. Whether they rehabilitate existing properties or build new ones, having ready cash to invest and economies of scale for renovation means large investors can make higher-quality SFRs available where other housing is scarce.

Photo courtesy of Center Creek Capital Group.

Is it investor activity or other factors stifling prospective first-time buyers?

At the same time, some critics have raised concerns that investors could crowd out prospective first-time homebuyers. While there is some evidence that home prices rise in areas where investors are more active, it’s hard to determine whether such increases are the result of investor activity or a correlation.

Other issues can more significantly complicate homeownership, particularly for renters with lower incomes and credit scores. One large SFR investor, the Amherst Group, reported in 2021 that 85 percent of its SFR tenants would not qualify for a traditional mortgage based on income and credit score limitations.

Responding to the New York Fed’s annual Survey of Consumer Expectations in February of 2025, almost 67 percent of renters said they believed it would be somewhat or very difficult for them to obtain a mortgage. While the majority of renter respondents said they would prefer to own, just under 34 percent said they would probably buy a home in the future.

“I’m a huge fan of the build-to-rent model. We have a housing supply shortage, so why shouldn’t we encourage building? For institutional investors, it ends up being more cost-effective, and it produces supply where it doesn’t otherwise exist.”

– Laurie Goodman, Urban Institute

There are also signs of strain among lower-income mortgage holders. Mortgage delinquency rates are rising, with the most pronounced increase among borrowers in the lowest-income ZIP codes.

While the single-family homes investors buy may sell for lower prices, these houses often require significant rehabilitation. Even if they can afford to buy that home, lower-income households are less likely to have the additional money needed to renovate. A single expense shock, such as the cost of a new roof or water heater, can push these households over the financial edge.

SFRs are an important option for households like these and others that want to live in single-family homes but can’t afford to or don’t want to own. Some investors are now pivoting away from purchasing existing single-family homes and toward the build-to-rent (BTR) model, increasing the inventory of new single-family rentals on the market.

“I’m a huge fan of the BTR model,” said Laurie Goodman, Urban Institute fellow and founder of the organization’s Housing Finance Policy Center. “We have a housing supply shortage, so why shouldn’t we encourage building? For institutional investors, it ends up being more cost-effective, and it produces supply where it doesn’t otherwise exist.”

What happens when SFR investors sell?

SFR investors often buy and sell houses according to market incentives. When economic tides shift, investors may want to quickly sell off a large portfolio of homes en masse, in part to benefit from tax advantages. Such bulk sales can significantly impact the neighborhoods where those investors own larger concentrations of properties.

“But individual homebuyers are not in a position to say, ‘Sell me 10 homes or 50 homes,’” said Starling of the Minneapolis Fed. “That’s where the intermediary system needs to be in place.”

Starling is referring to one way some communities, organizations, and impact-focused investors are adapting what works in the typical investor SFR model. They are testing approaches that center community, affordability, preservation, and housing choice. And as institutional investors increasingly sell off their SFR portfolios, these small but growing models like those from Land Bank Twin Cities, Center Creek Capital Group, and Grounded Solutions Network featured in the slides below may offer more sustainably affordable options for lower-income households to buy and rent single-family homes.

The land bank approach: Returning affordable homeownership opportunities to residents

Slide 1 of 3

A 3-bedroom North Minneapolis single-family home renovated and for sale at an affordable price with down payment assistance available for income-qualified buyers. Part of the Brick by Brick initiative, Land Bank Twin Cities acquired the house from an investor portfolio. Land Bank loaned more than $200,000 in rehabilitation financing to local nonprofit developer PRG, Inc. to renovate the home and complete energy efficiency upgrades.

Photo courtesy of Land Bank Twin Cities.

The diverse, lower-income neighborhoods of North Minneapolis have contended with multiple housing challenges since the late-2000s housing crisis. Amid the 2008 market crash, many families lost their homes to foreclosure and forfeiture. Then, in 2011, a tornado tore through the community. Large, out-of-state investors bought up many financially and physically distressed homes at the time—and now they are selling them.

Enter Aarica Coleman and Land Bank Twin Cities. Through its innovative Single-Family Investor-Ownership Intervention (SFIOI) pilot program, Land Bank hopes to reclaim these single-family homes as sustainable homeownership opportunities for community residents.

“Land Bank is a social impact real estate and finance intermediary,” said Coleman, Land Bank’s president and CEO. The nonprofit organization acquires and holds properties to prevent speculation and serve community goals. It also offers loan products for the acquisition, development, and rehabilitation of affordable housing units.

In the case of the SFIOI program, 80 investor-owned North Minneapolis houses were set to be sold off as part of a larger portfolio in 2023. Land Bank purchased 11 and sold them to local emerging or nonprofit developers, who are rehabilitating them. The developers plan to sell the renovated properties as affordable homes to local buyers earning 80 percent of the area’s median income. For Coleman, the focus on affordable homeownership is particularly important in this case.

“A healthy economy consists of renters and owner-occupants. I’m recognizing that what it comes down to is choice. When we feel like that choice—whether for an investor to purchase, an owner-occupant to purchase, or a renter to rent—is taken away, we have problems. The most important thing is decent, stable, dignified housing that is affordable to the people living in it.”

– Aarica Coleman, Land Bank Twin Cities

“It’s owning your own home that provides wealth,” she said. “We’re going to take this investor portfolio and sell it for affordable homeownership, prioritizing first-generation, first-time homebuyers.”

When the homes sell to new owners, the purchase capital will return to Land Bank to be reinvested in other community projects. Additionally, Land Bank provided $1.75 million in equity investment to enable another organization, Brick by Brick, to purchase and rehabilitate other properties from the same investor-sold SFR portfolio.

Though these particular Land Bank initiatives are homeownership-focused, Coleman said it’s important for local neighborhoods to also include high-quality, single-family rental home options for residents who prefer them.

“A healthy economy consists of renters and owner-occupants,” she said. “I’m recognizing that what it comes down to is choice. When we feel like that choice—whether for an investor to purchase, an owner-occupant to purchase, or a renter to rent—is taken away, we have problems. The most important thing is decent, stable, dignified housing that is affordable to the people living in it.”

“Investors can be part of making more of that housing available,” Coleman noted.

“We know we need all the players, and we have to create space for that,” she said. “The way our country’s real estate market is designed, we still need the investors. We just don’t need them to play an outsized role.”

Slide 1 of 3

The impact investor approach: Giving renters the choice to grow in single-family homes

Slide 2 of 3

Construction underway at Center Creek Capital Group’s Highline workforce BTR community in Knoxville, Tennessee. Center Creek is expanding the development to include a total of 261 3- and 4-bedroom single-family homes and townhomes, all offered at rents affordable to households earning 110 percent or less of area median income. The community also includes a pool, clubhouse, gym, and dog park.

Photo courtesy of Center Creek Capital Group.

Center Creek Capital Group, which is based in Washington DC and invests in properties across the Southeast, is a mission-oriented, for-profit housing investor and developer. Center Creek pursues three housing investment strategies across more than 1,000 homes and counting: rehabilitated single-family rentals, single-family houses for sale from affordable to luxury price points, and built-to-rent homes. The market-rate and luxury homes in Center Creek’s portfolio help subsidize the price of the affordable for-sale properties.

“Our heart is in the affordable houses,” said Dan Magder, Center Creek’s founder and managing partner. “We have a responsibility to the people living in the homes and the neighborhood. That belief really informs how we have built up the company and how we go about what we do.”

Center Creek’s average single-family rental home measures 1,500 square feet and typically includes three or four bedrooms, off-street parking, and a yard.

“The average US home size peaked in the 2000s at around 2,700 square feet,” said Magder. “If you want to build more affordably, it requires smaller homes, lower building costs, and more efficient land use. We acquire a distressed house and build two or five new homes in place of it, which spreads the land cost across more homes. Then you can make the sale price or rent lower more naturally.”

Magder said the company pays attention to what best fits the needs and resources of each community. Some homes need garages for example, but in more walkable neighborhoods, parking is less important. In Center Creek’s BTR communities, central clubhouse buildings offer residents gathering spaces for classes, meetings, and student tutoring.

“We want people to stay longer because they see it as a home. We can get relatively lower-income people into relatively higher-income neighborhoods. They can rent where they couldn’t afford to buy. It’s more stable for parents, who can be part of their community. Kids stay in the school district longer. These are important things that we can provide in offering these houses as rentals. Why shouldn’t renters have that?”

– Dan Magder, Center Creek Capital Group

“We want people to stay longer because they see it as a home,” said Magder. “We can get relatively lower-income people into relatively higher-income neighborhoods. They can rent where they couldn’t afford to buy. It’s more stable for parents, who can be part of their community. Kids stay in the school district longer. These are important things that we can provide in offering these houses as rentals. Why shouldn’t renters have that?”

To more efficiently manage its properties and provide tenants with amenities, Center Creek is expanding its model to include more BTR. Unlike scattered-site houses, Magder noted that the BTR model allows for onsite maintenance staff who can attend to issues more quickly.

“If we treat our residents well, they stay in the house longer and they’re likely to take better care of it,” said Magder. “My repair bill will be lower, turnover will be lower, and I’ll have lower associated costs. That’s almost all I need to do to convince any investor, and we have a whole lot of impact investors who more fundamentally like what we’re doing.”

Slide 2 of 3

The shared equity housing approach: Retaining affordable single-family homes over time

Slide 3 of 3

A single-family rental home acquired from an investor portfolio in Minneapolis, Minnesota through the Homes for the Future initiative for eventual affordable homeownership.

Photo courtesy of Grounded Solutions Network.

In Grounded Solutions Network’s Homes for the Future model, the focus is on preserving affordable homeownership. Grounded Solutions seeks opportunities to acquire SFR portfolios where local shared equity organizations want to collaborate to implement a lasting affordability structure for the homes they buy.

Grounded Solutions works with the local partner to purchase the houses and then stays on as the properties’ asset manager. They hire a third-party property manager to handle maintenance and operations for the existing tenants, who are typically still living in the portfolio’s homes when they’re sold.

Existing renters pay stable rents. These renters are not required to buy the home or move out if they do not wish to buy, but they are made aware that they have the opportunity to purchase the home. If they express interest in buying, the program covers the cost of homebuyer and financial readiness classes provided through local partners. In the meantime, rental income helps pay down debt on the property.

The key element in the Homes for the Future model is an affordability clause. Once a prospective buyer is interested in owning the home, the organizations explain that to take advantage of a lower purchase price, that buyer must then commit that they will subsequently sell the home only for a similarly affordable price.

“Our focus is that the equity built and accumulated during the Homes for the Future ownership is then stewarded in the community over time, rather than an affordable homeownership model where there’s a single owner and then the home is returned to market.”

– Devin Culbertson, Grounded Solutions Network

In this way, the home remains affordable even as one buyer sells it to another. Instituted over multiple properties in a neighborhood, this approach ensures long-term affordability within the community overall. While this system limits price growth, moderate-income homeowners can still build meaningful wealth through modest equity gains over time.

“Our focus is that the equity built and accumulated during the Homes for the Future ownership is then stewarded in the community over time, rather than an affordable homeownership model where there’s a single owner and then the home is returned to market,” said Devin Culbertson, Grounded Solutions’ vice president of innovative finance.

As they lay out plans for eventually selling the homes they’re acquiring, the team intends to include a range of purchase price points. Some homes can be sold at higher prices to subsidize others offered to people with lower incomes.

Grounded Solutions made its first Homes for the Future investment in the Twin Cities in 2024 and has since expanded their work to Atlanta and Texas. Now they’re exploring how best to scale up the model.

“We think the best opportunities are not the 1,000-unit portfolio or the individual homebuyer,” said Culbertson. “It’s the investors in the middle that have 20 or 50 homes and need to sell them, but the regular market is just too slow. They’ve already doubled their money, so they’re willing to take a bit of a hit on current pricing to move on, and we need to be nimble to do that.”

“There’s a lot we’ve learned about the advantages of scale that institutional investors enjoy and what waits for our model when it gets to that scale,” he added. “But it’s also understanding the path that we have to walk to get there, because folks also want to see even more growth and progress from this approach.”

Slide 3 of 3

Evolving mainstream investor models for greater affordability and community benefit

As these organizations refine their strategies, profit-focused investors also are likely to continue evolving their role in the SFR market. In addition to expanding build-to-rent opportunities, the Urban Institute’s Goodman notes institutional investors can adopt policies and practices that would benefit SFR tenants.

“Size brings responsibilities,” she said. “In terms of the consumer, if you’ve got large size, there are certain things you can do more cheaply to enhance the tenant experience. It should just be expected that you’re required to do that.”

For example, institutional investors can report tenants’ rent payments to credit bureaus and provide tenants with clear, one-page lease summaries that lay out terms and fees. They can also accept Housing Choice Vouchers, which Goodman said many large investors already do.

Photo courtesy of Land Bank Twin Cities.

To further evolve the SFR model, institutional investors that have developed efficient maintenance services can provide those services to other investors for the benefit of their tenants. When ready to sell a portfolio, investors can also choose to sell their SFR properties to nonprofits, impact investors, and other mission-oriented organizations, instead of putting those homes on the open market.

At the same time, Grounded Solutions’ Culbertson noted that mission-oriented organizations can learn from investors, adapting strategies to scale up their approaches more quickly and effectively.

“If we think about scale of capital, operating latitude, decision making, and governance, I think we have to learn some things from the private sector in terms of how to be nimble,” he said. “We’re trying to get out of the lane of housing that’s administratively burdensome and not very cost effective to operate or build. We have to be open to some different operating and business plan paradigms that take a page from other books.”

Disclaimer: Libby Starling of the Minneapolis Fed serves on Land Bank Twin Cities’ Board of Directors.