Families and individuals often dream of homeownership. From their first home purchase, many begin to grow wealth that helps future family members climb higher on the economic ladder. It’s wealth that is passed down to new generations. Yet this dream has long been out of reach for some.

In the past, discriminatory policies and practices prevented many people of color and lower-income earners from accessing mortgage loans. Even today, many of the factors that lenders consider in estimating who could reliably repay a mortgage loan keep some out of homeownership.

Who runs up against these barriers most often in a state or county when they apply for a mortgage? Are applicants who want to purchase a home in certain cities or neighborhoods more likely than others to face those barriers? Answers to these questions are now easier to find with the freshly updated Home Mortgage Explorer from the Federal Reserve Banks of Cleveland and Philadelphia. The online dashboard allows you to quickly learn about, compare, and share mortgage-data patterns for places across the US.

Identify neighborhood-level impacts of who can get a mortgage

To understand where and why there are wealth gaps in the US, it’s important to know who can and cannot access homeownership. Loan applicants with lower credit scores or a lack of credit history often struggle to secure mortgage loans, for example. Having a higher amount of debt compared to one’s income is another barrier. So is not having enough money for a down payment on a home.

The Home Mortgage Disclosure Act, or HMDA, requires many mortgage lenders to record and report certain information about their applicants. The lenders must do this even if they end up denying a mortgage loan application. The information reported includes the race, ethnicity, and gender of applicants, and the loan amount requested.

Even if a loan application is ultimately denied, lending institutions must report the reason why. Combining this information for all loan applications in one neighborhood, city, or state provides valuable insight. It reveals patterns in places where certain borrower characteristics and application approvals or denials are more common.

“The Home Mortgage Explorer tells us the story about who was able to get a home mortgage loan in the years after the Great Recession, including during the COVID-19 pandemic.”

Kyle DeMaria, Philadelphia Fed

Quickly find mortgage information and trends for US cities, counties, and states

HMDA data provide powerful information if you want to understand where it’s been harder for people to get a mortgage loan. Historically, though, it’s been difficult to access and work with this information. That’s because researchers typically need special software and training to sort through the giant datasets made available through HMDA. So even though the datasets are public, they are hard to use for most people outside of a research setting.

Cleveland and Philadelphia Fed researchers wanted to make it faster and easier for anyone to find the mortgage information they need. They created the Home Mortgage Explorer, or HME, to smooth out and speed up the process.

“We want to make it accessible to people who don’t have the ability or time to do their own analysis,” said Lisa Nelson, assistant vice president at the Cleveland Fed. “All the work is done for them for the indicators that we have.”

Nelson and Kyle DeMaria, community development research associate at the Philadelphia Fed, worked to enhance the original 2016 tool over the past year. The HME now offers a wider range of mortgage information across several categories for states, counties, and cities across the US from 2010 to 2021.

“The HME tells us the story about who was able to get a home mortgage loan in the years after the Great Recession, including during the COVID-19 pandemic,” said DeMaria.

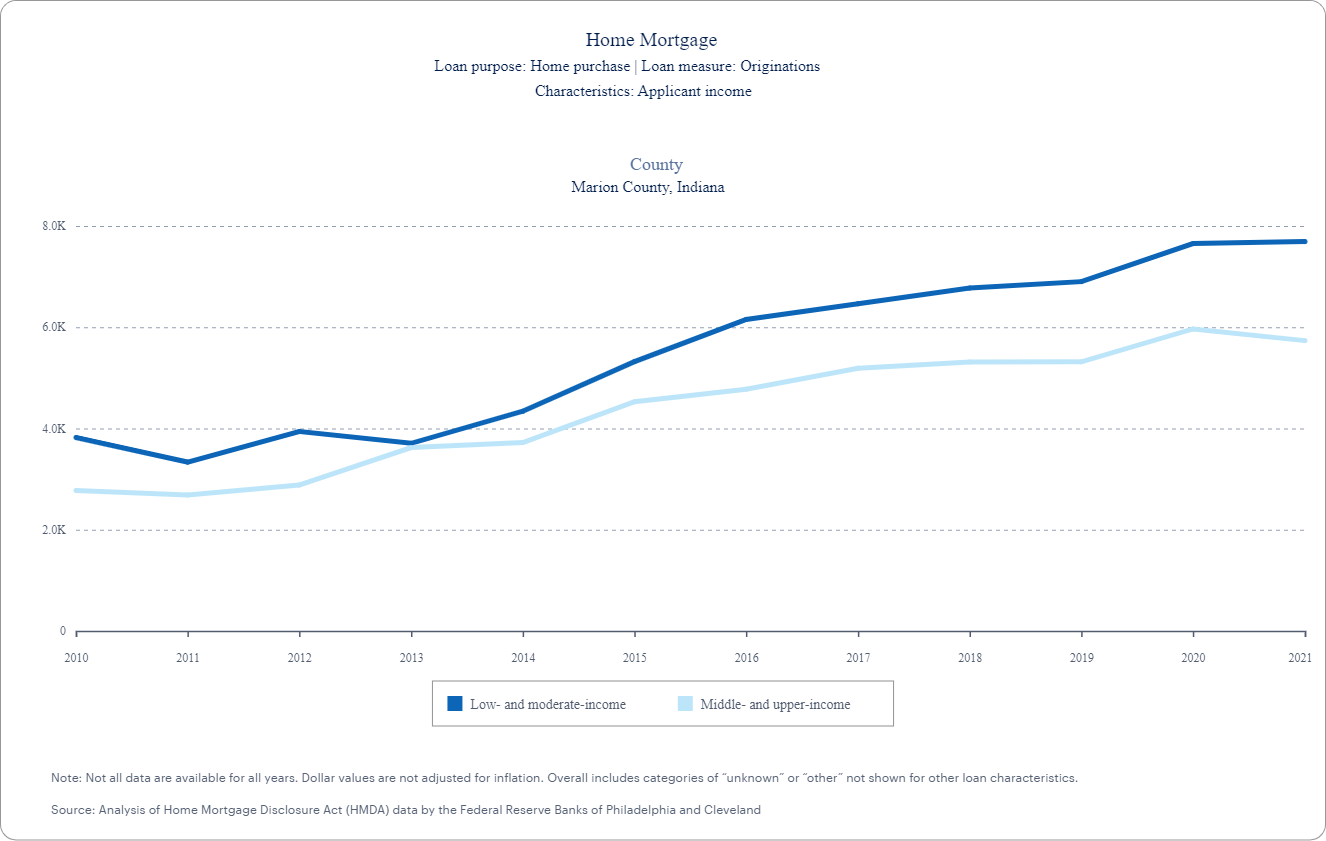

In the HME dashboard, enter your search request. For example, you might want to know whether the number of mortgage loans approved in Marion County, Indiana, for lower-income borrowers went up or down between 2010 and 2021. With a few quick selections, the HME provides the answer in an easy-to-read chart.

Home Mortgage Explorer chart example

Local mortgage origination and denial context at the ready

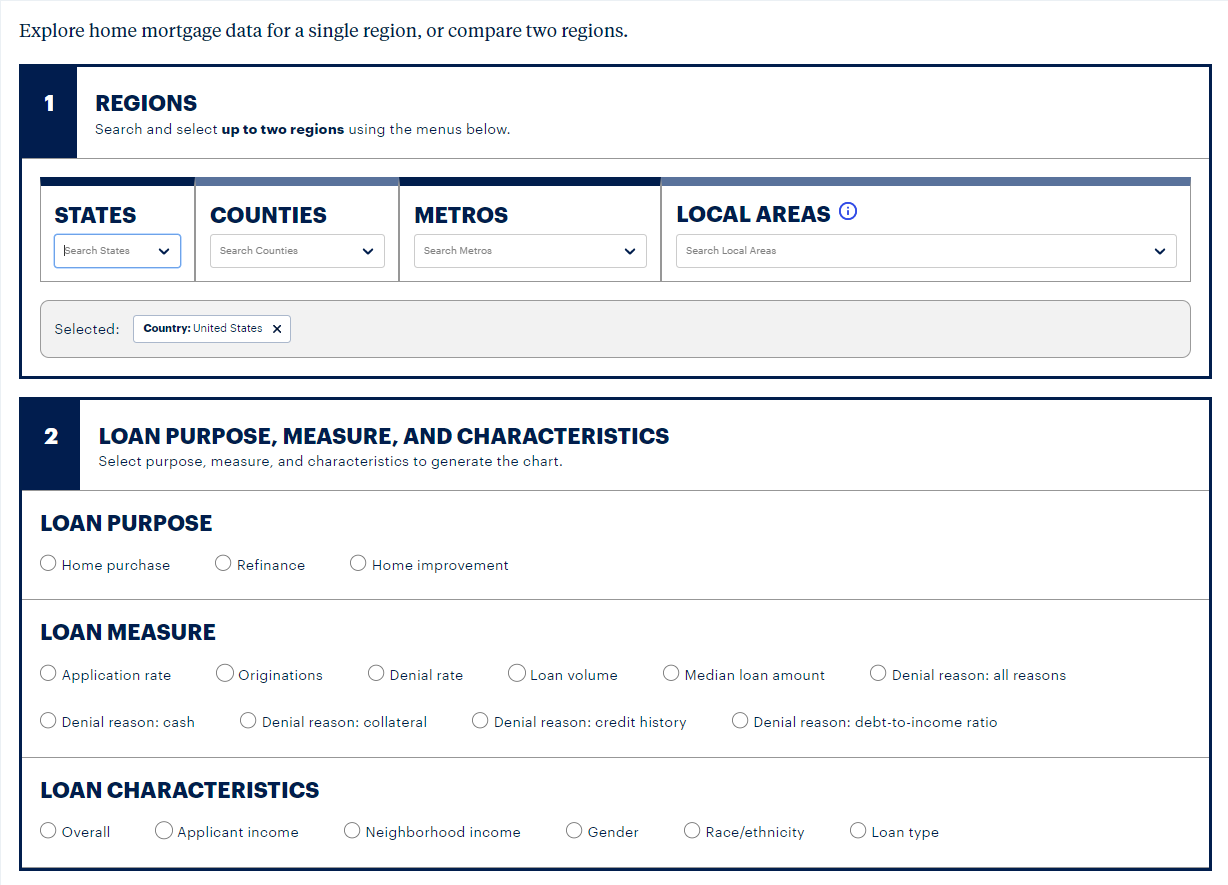

The refreshed HME dashboard now includes options to search the data by race and ethnicity, income, and gender. “People are looking for that information but we didn’t have these data in our previous tool. The current version allows you to sort by those categories,” said Nelson.

It also offers place-specific mortgage information at the county level, and even down to a local level for sections of many larger cities. Want to share the information you find in your own article or presentation? Download cleanly formatted charts for quick placement.

Home Mortgage Explorer interface

DeMaria added that policymakers and community organizations are also likely to find value in the HME. “If someone were trying to start a down-payment assistance program, for example, they could look at how often people are denied for cash reasons. That would be a way to help bolster their program or their application for a grant.”

He and Nelson expect it could be useful as well to those writing on a deadline about mortgages and homeownership. “This would be a great way for a journalist to quickly get a data point that provides context for a story,” said DeMaria.

Closing the homeownership gap

Both Nelson and DeMaria caution that the HME should not be used to draw conclusions about bias in the mortgage-lending process. It also cannot shed light on every factor that goes into a particular mortgage decision. However, it can shed light on disparities in mortgage application outcomes.

“If there are disparities in who is receiving a mortgage, that affects who can use homeownership as a wealth-building tool,” said DeMaria. “That then has consequences across generations on who can pass a home along to their children.”

He continued, “One way that we can reduce the homeownership gap is by understanding who is being denied a mortgage and the most common reasons for those denials.”

That’s where the HME can help. It searches the data for you so you can get the information you need fast. That makes it much easier to find out where people have had a harder time getting a mortgage and some of the reasons why. With the HME, that important information now is in the hands of those who can discuss and act on it to help more people achieve homeownership.

Check out the Home Mortgage Explorer to start using the data yourself.